Business owners know how crucial it is to get paid for the hard work they put in. When invoices are left overdue and unpaid, it can cause cash flow problems that threaten a business’ ability to operate and serve its clients, and understanding how to collect past due invoices and unpaid bills is essential to ensure your businesses survival.

Let’s dive in to Monetaria’s 5 step guide on how to collect unpaid invoices from customers:

Step 1 — Identify Overdue Invoices:

First things first, you’ll want to keep track of those pesky unpaid invoices. With the help of your in-house bookkeeper or accounting software of choice, it shouldn’t take too long once a month to identify past due accounts and unpaid bills that need to be collected.

Step 2 — Send a Courteous Reminder Email:

We’re all human, and sometimes things slip through the cracks. So, having identified which customers have outstanding invoices, start with a courteous follow-up email to gently remind the client about the overdue payment, in a personal way that offers them the benefit of the doubt and dignity to make it right. Providing multiple payment options and ensuring a smooth process can make a significant difference in ensuring you get paid.

Related: A Step by Step Guide to the Commercial Debt Collections Process

Step 3 — Reach Out via Text or Social Media:

In case the first email gets overlooked, after a number of days, you can take a slightly more direct approach to get in touch with the client who has overdue invoices. A quick text or a message on social media to the right person often grabs their attention and gets the ball rolling.

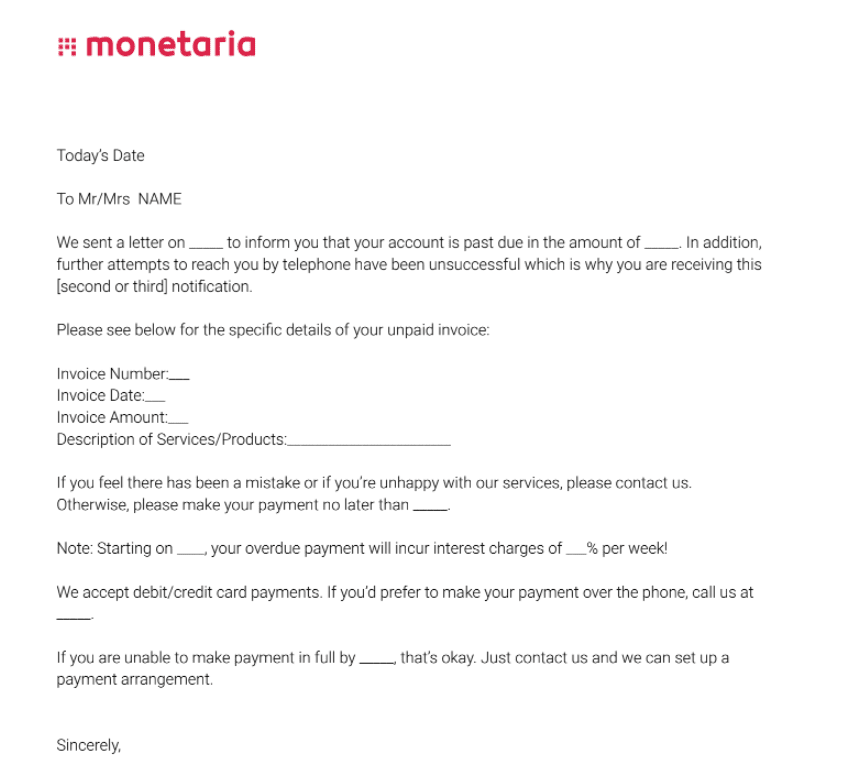

Step 4 — Send a Final Reminder Email and Make a Final Phone Call:

If the previous steps didn’t yield results and it appears the person is ignoring your emails and hoping you fade away , shift gears and send a more assertive email. Lay out all the accommodations you have made for them and the many ways you’ve tried to connect with them to sort out the issues. Tell them that because of the unpaid invoice and lack of communication, you are now taking steps to apply late fees, stopping all work until they pay their overdue bills, or sending them to collections.

Even while taking a tougher approach, you can still offer methods of reconciliation and opportunities to reach a mutually beneficial outcome for both parties.

Step 5 — Pursue Legal Means and Debt Recovery Solutions:

If all else fails, it’s time to step up the game. If the payment is still outstanding after your best efforts to sort it out independently, it might be time to accept that the client won’t come through without getting other people involved. In this case, businesses usually contact a third party debt collections agency to handle the matter further.

Related: How to Recover Financial Control with Debt Collection Agencies

Remember, communication and offering solutions are key throughout this process. If doing it in house isn’t working, debt recovery specialists like Monetaria are always here to help you collect unpaid invoices, outstanding bills, and all the money owed to you.

We’re happy you found this article informative! Go back to our blog page to find more tips, tricks and guidance on collections, to ensure your business gets paid.

If you have unpaid debts that need to be recovered, commercial debt collection may be a good option for your business. A commercial debt collection agency can help you with the process of recovering past-due accounts and provide guidance on best practices for managing accounts receivable.

Led by a team of experienced commercial debt collection attorneys, Monetaria Group has helped hundreds of businesses recover and collect their outstanding debts and payments. Schedule a FREE consultation with our expert team to see how we can help you recover your money today!