Running a successful business is about keeping your accounts receivable above water. When you see those relationships start to sink, the effects on your cash flow could be devastating.

So you’ll need to implement the right strategies to make sure your customers pay on time. When you do, you’ll ensure that your cash flow stays in the green and your stress levels stay low.

When customers don’t pay, you must shift your collection efforts into a new gear to recover any outstanding amounts. Collection letters are an invaluable tool you can use to get payment from customers while still preserving your relationship with them.

But where do you learn how to write a collection letter? What information should you include? When should you send it?

At Monetaria, we live and breathe collections. Below, we’ll answer your collection letter concerns in detail. As a bonus, we’ll give you a collection letter template you can use in your efforts.

What Is a Collection Letter?

Before we get into the details, let’s recap what a collection letter actually is. Simply put, a collection letter is a written notification that you send to a customer to inform them about their due payments.

Typically, a collection letter may include payment reminders, inquiries, warnings, or notifications of possible legal action to be taken against a customer if they fail to pay overdue amounts promptly. Ultimately, if done right, collection letters help you to get paid while leaving the relationships with your customers intact.

What Makes a Collection Letter Effective?

Your relationship with your customer begins with effective communication. Staying honest is key. Communication typically starts by collecting the customer’s information and also providing them with a contract or conditions of sale that outlines your payment terms.

However, it may happen sometimes that customers don’t pay. And here, collection letters are another vital part of communication and a key tool that you can use to recover outstanding accounts. These letters are so so effective because they:

- notify customers of outstanding accounts

- demand payment from customers

- indicate the steps required to get back on track

- serve as notifications of the steps you’ll take if they fail to make payment

Heads up: to be effective as a tool in your collection efforts, there’s some information you need to include and mistakes to avoid.

What Information Should You Include in a Collection Letter?

Now that we’ve seen what collection letters are and why they’re effective, let’s look at the key information any effective collection letter should contain:

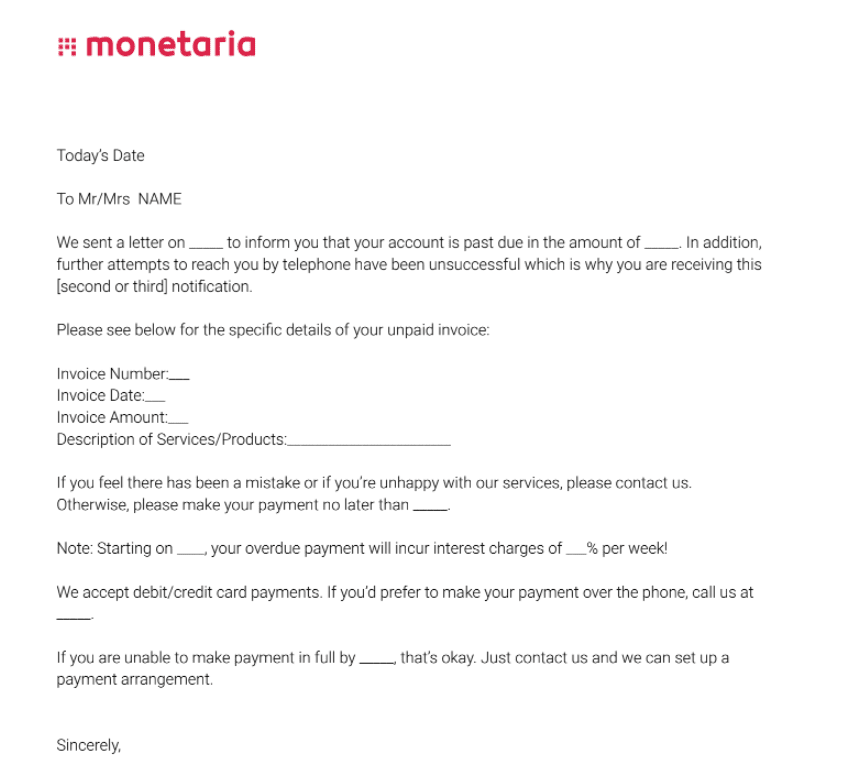

- Company details. You must include your contact details on the collection letter including your address, telephone number, email address, and website if you have one. This is simply to make it easier for the customer to contact you.

- Amount owing. You’ll have to include the exact amount owing. Ideally, you should include it in two places in the letter and it should be clearly visible.

- Due date. It’s important to always include the date when the balance was due to be paid.

- Invoice or account number. By including the account number, you’ll ensure that your customer knows exactly what account you’re referring to, so you can eliminate disputes later on. Including the account number also helps you keep track of the collection letters you’ve sent and follow up on payment. If you have a written contract with your client, also include reference to the contract and the date it was executed.

- Call to action. This is one of the most important parts of the collection letter and aims to appeal to your customer to pay the outstanding amount. Here, it’s a good idea to include different methods of payment so that your customer can choose the most convenient one, which, in turn, increases the possibility that they’ll pay.

- Thank you. Although it may sound strange to thank the customer, it goes a long way not only to increase the possibility that the customer will pay, but also shows professionalism and that you’re willing to maintain the relationship with the customer.

The Four Types of Collection Letters

The First Collection Letter

You’ll typically only send the first collection letter after you’ve tried to contact the customer by phone or email, and you couldn’t get a hold of them. In some instances, you’ll also send the first collection letter if you’ve gotten hold of the customer, but they failed to make a payment arrangement in respect of the overdue amount.

Keep in mind, though, that you should send the first collection letter no later than 14 days after the due date.

The second Collection Letter

Before you send the second collection letter, you should try to contact the customer again to find out whether they got the first collection letter and if they want to make a payment arrangement. If you can’t reach the customer or you do, but they fail to make an arrangement, it’s time to send the second collection letter.

Although the first and second collection letters convey much the same message, the main difference between the two is that you’ll make mention of the previous collection letter in the second letter.

The third Collection Letter

Once you’ve sent the second collection letter, you’ll once again try to contact the customer by phone. If you can’t get hold of them and they’ve made no attempt to contact you after the initial two letters, you should send the third collection letter.

Like the second collection letter, you’ll refer to the first two letters and the fact that all attempts to recover the outstanding balance from the customer have been unsuccessful. Here, it’s also advisable to send the letter by certified mail as this requires that someone sign for the letter, which gives you proof that it was received.

The fourth Collection Letter

By the time you get to the fourth collection letter, it should be clear that the customer is either unwilling or unable to pay the outstanding amount. As a result, you’ll also use the most assertive language in this letter while still remaining professional.

Like the third collection letter, you’ll state that previous letters have been sent and all attempts to collect the outstanding amount have been unsuccessful. Likewise, you’ll also send this letter by certified mail to ensure that you get proof that it was delivered and received.

Common Mistakes To Avoid

Remember, the ultimate goal with the series of collection letters is to recover any outstanding amounts from a customer while maintaining a good relationship. Although you now have some guidelines as to what information to include and when you should send the letters, there are some things you shouldn’t do.

Considering the above, it’s vital that you don’t:

- Use harsh words in the letter and rather keep it professional.

- Harass customers for payment. Although, in some cases, customers won’t pay, it’s always best to assume that they will.

- Send text messages to customers. It’s always better to use collection letters that are formal and professional, and which provide you with proof that they were delivered and received.

- Communicate with customers through social media. As stated above, you want a record of the correspondence that you’ve sent to the customer and the proof that they’ve received it. With social media, this is unfortunately not very easy to keep a clean record.

Download collection letter templates

With our free template, you’ll be able to send one or more collection letters to the customer to get your cash flow back on track.

The Bottom Line

When you want to optimize the cash flow in your business, you must implement the right strategies to ensure that your invoices and outstanding balances get paid on time, every time.

Hopefully, this post helped illustrate what information you should include in a collection letter and when it should be sent.

To find out more about collections, our services, or to download our collection letter template, visit our website or get in touch with us for more details. Monetaria Group is a New York-based B2B collections company that helps both small and medium businesses with their B2B collections.